Cattle imported from Mexico have become a significant part of the U.S. beef supply, raising the stakes for the Trump administration’s battle against an outbreak of New World screwworm at a time when U.S. cattle production is in a down cycle.

Consumers are feeling the pinch of higher beef prices due to the reduction in cattle supplies. Last week the choice boxed beef price, which tracks with retail beef prices, reached $367.55 per hundredweight, up 16.8% year-over-year, and a new record excluding a brief COVID-19 price spike.

Ranches and feedlots in the southwestern United States that rely on Mexican cattle for their normal operations also are being hurt significantly by disruptions in imports.

As of May 1, the three states with the largest year-over-year declines in cattle on feed were all border states: Arizona (down 9.1%, or 23,000 head), California (down 7.6%, or 40,000 head) and Texas (down 6.5%, or 180,000 head). Like any business, feedlots not stocked to optimal or typical levels are less efficient than they otherwise could be.

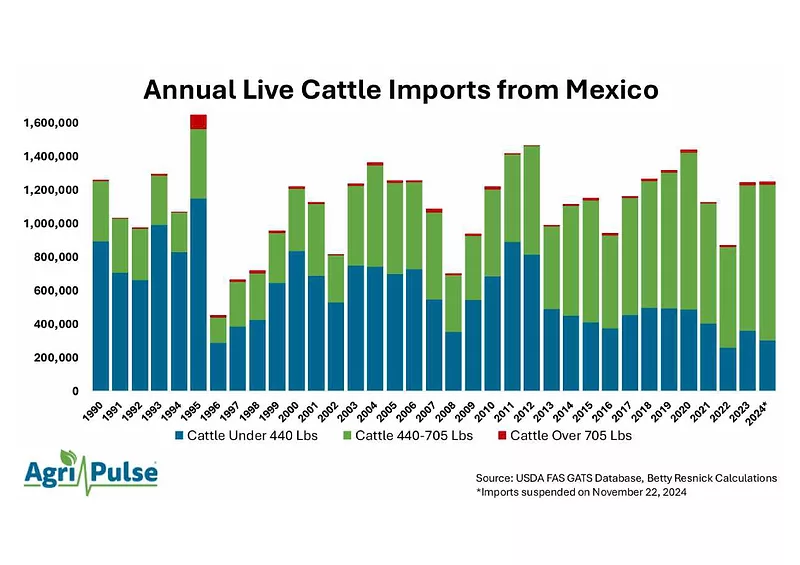

Over the past decade the U.S. has imported an average of 1.17 million head of cattle from Mexico annually, accounting for 60% of U.S. live cattle imports. Even though imports of Mexican cattle were suspended for the last five weeks of last year due to the screwworm outbreak in southern Mexico, 2024 was still an above-average year for imports of Mexican cattle. About 1.25 million head worth $1.3 billion were imported, the most since 2020.

For context, live cattle imports represented 2.7% of the total value of agricultural products imported by the U.S. from Mexico in 2024.

Mexican cattle imports tend to be feeder cattle, with the overwhelming majority entering the United States at under 320 kilograms, or 705 pounds. Depending on the weight at import, the cattle may be placed on pasture, put into a stocker program or sent directly to a feedlot.

Mexico has a comparative advantage in cow-calf production due to lower labor costs, mild winters and vast forage land. The United States has a comparative advantage in feedlots, with ample feed supplies and access to capital.

Since 2000 approximately one in six calves born in Mexico, or 15.5% of its production, is exported to the United States as live cattle. From the U.S. herd perspective, Mexican imports are, on average, equivalent to 3.3% of the nation’s calf crop, a small but substantial part of the supply chain.

Impact of Border Shutdown

NWS was contained to South America for nearly 20 years, but an outbreak started in 2023 that quickly spread northward through Central America, in part due to increased cattle movement.

It’s easy to be “in the know” about what’s happening in Washington, D.C. Sign up for a FREE month of Agri-Pulse news! Simply click here

USDA suspended imports of Mexican cattle for 10 weeks after the Mexican government informed the department Nov. 22 that NWS had been found in a cow in southern Mexico. Imports resumed on Feb. 1, but on May 11, USDA again shut down the importation of live cattle due to advancement of NWS to Oaxaca and Veracruz – a mere 700 miles from the U.S. border.

Theoretically, during the freeze in cattle trade, Mexican-born calves could stay on pasture in Mexico and then be imported into the U.S. once NWS protocols were established and the border reopened. If that were the case, the U.S. would have expected to have seen cattle imports quickly rebound and potentially surpass average monthly imports to make up for the lost trade during the pause.

However, that has yet to occur. Instead, from February through April cattle imports were well below the average imports of those months in the previous five years. Since the first shutdown from late November through April, the U.S. has imported 391,032 fewer cattle than would be expected, compared to the five-year average.

From December through April, and thus not accounting for the second shutdown starting on May 11, imports are down 66% compared to previous years. If a sustained border closure occurs, the cattle industry will see its lowest import total from Mexico in several decades.

The reduction in imports after the border reopened was likely caused in part by a reduction in available ports of entry from nine to five (including only one in Texas) due to new NWS protocols.

But the theory that cattle would simply stay on pasture in Mexico before export to the U.S. has some merit. Even though there are still hundreds of thousands of cattle missing from the U.S. supply chain, the relatively few cattle imported while the border was temporarily reopened in the months of February, March and April were heavier than the same months in 2024.

Economic Impacts

The Jan. 1 U.S. cattle inventory was at a 74-year record low of only 86.7 million head. Despite years of record beef and cattle prices, demand has stayed strong. With such a tight market, even a marginal loss of 3% to 4% of feeder cattle will continue to push the price of cattle, and beef in the grocery store, to new highs.

Boxed beef prices can be affected by a variety of factors and tend to spike in May as grilling season ramps up, but they also rose after the import suspensions were imposed in November and May and declined after the initial suspension was lifted in February.

The longer-term effects of the import suspensions are hard to predict in what is a fluid situation.

The shutdown of the border may encourage more cattle to be slaughtered in Mexico, leading to more domestic competition against U.S. beef exports to Mexico (and in other markets).

It could also lead to further development of finishing capacity within Mexico and smaller Mexican producers going out of business, leading to long-term changes in the market.

Betty Resnick is an agricultural economist based in Monterey, California. She formerly was on the staff of the American Farm Bureau Federation.

For more news, go to Agri-Pulse.com.