WASHINGTON, Feb. 1, 2017 - An update on American farm families and their health insurance is a two-part story. On the one hand, with probably the final annual signup under the Affordable Care Act now expired, a lot of low-income farm families face possible loss of health insurance or at least the critical tax credit that makes it affordable for them.

On the other hand, most middle- and high-income farm households still want what the ACA promised: affordable care. Like the vast majority of Americans, they’ve endured mounting (or stampeding) premiums and deductibles, along with shrinking choices of health insurers, across the three years of ACA enrollment – even though many have benefitted from ACA rules that, for example, require policies to cover pre-existing conditions and cover students in family policies to age 26.

David Sanchez, a Chama Valley, New Mexico, rancher and active member of the Northern New Mexico Stockmen’s Association, says he is fortunate his pension includes health coverage, but many family members aren’t so lucky. “We are talking about U.S. citizens, family members, who are part of the farm and ranch and business community in this rural area. We have kids who work on the ranch and are not able to obtain insurance because the premiums are significant, and then with what they could buy, the deductibles are [very high]. It’s asinine to have to come up with $10,000 to $20,000 up front plus deductibles.”

Sanchez reports: “My son works on the ranch. He tells me, ‘I can’t afford it, and it’s not worth it.’ They need to offer something that makes sense.”

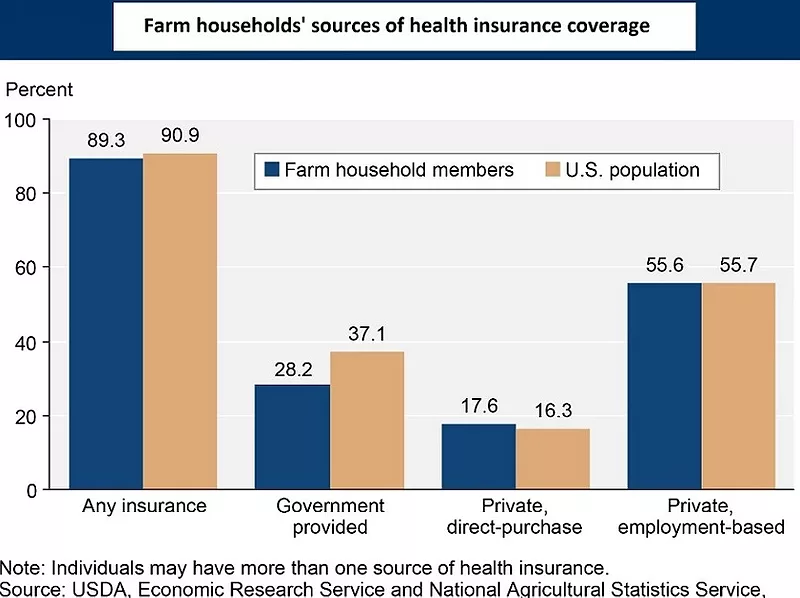

Considering that only about 20 percent of farm household income is generated by farm operations, it’s no surprise that farmers’ health care coverage differs little from that of Americans overall, as USDA’s Economic Research Service found in its recent report of 2015 farm household health insurance coverage. Health insurance is very typically a priority for one or both spouses when seeking off-farm employment. So, while less than 18 percent of all farm family members are covered by individual policies, 89 percent of them have some level of coverage and 56 percent of all farm household members are covered by employer-sponsored plans (see chart).

Farm operator households, however, do have fewer members in poverty and fewer retirees than the public at large, so nearly a third fewer farm households collect Medicare or Medicaid benefits than do Americans generally.

Low-income farm families, however, are among the 11.5 million Americans that have enrolled in federally supported health coverage exchanges and among the 15.7 million added to free Medicaid or related Children’s Health Insurance Program since ACA sign-ups began in 2014. Thirty-one states and the District of Columbia took ACA’s federal-state cost-sharing option to accept Medicaid enrollments from all households with income below 138 percent of the federal poverty level (FPL).

Meanwhile, health insurance through the exchanges, available in all states, offers income tax credits against the costs of health insurance premiums when individual or household income is less than 400 percent of FPL. The tax credits are based on income. As examples, a 60-year-old non-smoking single with annual income under $47,500 would get tax credits rebating half of the $770 monthly premium of an average U.S. plan, according to the Kaiser Family Foundation (KFF) online estimator. And a 60-year-old non-smoking couple with household income under $64,000, meanwhile, could write off two-thirds of their $1,500 monthly premium.

Besides that, Jennifer Sullivan, a vice president of the ACA-promoting Enroll America, points out, “The way the cost sharing and subsidies are structured (in the exchanges), consumers ultimately are very well insulated from price fluctuations.” The premiums are capped at a percentage of income so they don’t rise no matter how much the insurer might jack up premiums. A 40-year-old nonsmoker with $30,000 income in the Minneapolis area, for example, buying a standard “silver” policy will pay about the same $207 a month as last year, even though his premium shot from $235 to $366, up 55 percent since 2016, the KFF estimator says.

Bargains like that benefit small farm operators such as Larry and Yolonda Bailey, vegetable and specialty-crop growers on a small farm near Brainard, Nebraska. They didn’t buy health insurance and rarely saw a doctor until they were able to enroll themselves and their disabled adult son in federal exchange coverage in 2014.

Their plan includes an affordable $1,500 annual family deductible and small copayments for some clinic stops. No premium. “We just don’t make very much money. We live with very little safety net,” she says. Larry works sometimes for another farmer as well, but all their income is subject to self-employment taxes. “When it comes to money for doctors, no, we do not have it.”

After two years with insurance, Yolanda contracted Lyme’s disease, plus she ended up in surgery to remove a tumor from her kidney. Her main cash-out for all the care was the $1,500 deductible, on which she is still making payments. “That’s the thing – I don’t know what I would do” without the low-cost coverage,” she says.

Keep up with ag and rural policy and energy news as it happens. Sign up for a four-week free trial of Agri-Pulse.

Jordan Feyerherm, who advocates for and writes about rural health care at the Nebraska-based Center for Rural Affairs, says of Yolonda: “It seems like her experience is pretty common for small-time Nebraska farmers.”

But the ACA price protection doesn’t do much for farmers and ranchers who must buy their own coverage. “If you don’t fit within the exchanges, you get nothing,” says Rudy Arredondo, president of the National Latino Farmers and Ranchers Trade Association. “Then, the closest thing to having access to health care is community health centers – if you are lucky enough be within a center’s (service area).” For many middle-income folks, that means “you have to be proactive in order to avail yourself of health care,” he says.

Keldron, South Dakota, ranchers Mike and Danni Beer are among those continuing to wrestle with the soaring prices of coverage. Danni, former president of the U.S. Cattlemen’s Association, checked her annual health care premiums (no dental) for them and their four children, which jumped by 73 percent from 2012 to their 2017 rates, topping $14,000.

Keldron, South Dakota, ranchers Mike and Danni Beer are among those continuing to wrestle with the soaring prices of coverage. Danni, former president of the U.S. Cattlemen’s Association, checked her annual health care premiums (no dental) for them and their four children, which jumped by 73 percent from 2012 to their 2017 rates, topping $14,000.

The Beers’ ranch is an hour’s drive to the nearest emergency room. But, fortunately, she says, they’ve had good health and haven’t needed a lot of care, nor have they spent their $2,500 per person deductible nor the $5,000 out-of-pocket family limit. That is, until her son had an accident last year, which involved “an emergency room visit, air ambulance, surgery and hospital stay.” The ambulance charge alone was $45,000, she said, so total costs would have gone through the roof without the insurance.

#30