A turbulent couple of months for meatpackers and their employees has placed a fresh focus on the industry’s capacity to process the chicken, pork and beef on American dinner plates.

While factors unique to each meat category prevent a one-size-fits-all solution, the conditions brought to light by COVID-19 have served to amplify existing issues in the processing industry. Where processing capacity expansion was being considered before, it’s now sorely needed; where inventory was needed to catch up to capacity before, it’s now a race to build herds up to the kind of quantity to keep plants humming.

The drop in USDA’s estimated slaughter numbers is not as pronounced now as was several weeks ago, when plants were forced to close as COVID-19 hit their workforce.

At one point, experts estimated protein processing was operating about 40% short of maximum capacity. In recent days, USDA’s daily livestock slaughter figures show a loss of closer to 10% to 15% of capacity as plants come back online. On Monday, USDA estimated the nation's daily beef slaughter at 110,000, about 90% of the 122,000 head slaughtered on the same day a year ago. The pork sector offers a similar story; Monday's estimated slaughter was 403,000, about 85% of the 465,000 slaughtered the previous year. The sheep industry is a little further behind, harvesting 8,000 head compared to the previous year's 10,000.

But as facilities open their doors and turn on the complex machinery needed to make a modern-day packing plant work, it’s anyone’s guess how long it will take to achieve the kinds of output measured just a few months ago.

“The popular view of the marketplace has been that we could get to 85% to 90% of slaughter, and beyond that, with these changes in the spacing requirements, it’s going to be a tough go from there,” Don Close, a senior animal protein analyst with Rabo AgriFinance, tells Agri-Pulse. But he also sees some reason for optimism that the numbers could creep a little higher.

“Those processors, and it doesn’t matter the species, what they are absolute masters of is driving efficiency into a system,” he added. “I think as they get ramped up with staff, they see what their obstacles are for product flow and human flow, they’re going to work that problem out.”

According to Close, “the argument was already in place that (the beef industry) probably needed more” slaughter capacity, something the COVID-19 pandemic further emphasized. But the virus has also led to calls for a reshaping of the very sector that supplies the nation’s beef and pork.

Longtime critics of the so-called “big four” packers in the beef industry (JBS, Tyson, Cargill, and National Beef) have said the coronavirus outbreak underscores the need for more small to medium packing plants that sell their products locally rather than the handful of giant facilities that market their products all over the world. Close is skeptical that’s the right approach, and Purdue University economist Jayson Lusk says it “doesn’t fix some of the problems we’ve seen.

Jayson Lusk, Purdue University (Photo: Joy Philippi)

“That extra capacity is costly,” Lusk said in an interview with Agri-Pulse. “You don’t want to build a multimillion-dollar facility just to have it sit there not running full. No investor can withstand that kind of economic prospect. So the economics in the system are such that it doesn’t make sense to build a plant that’s not going to be able to run close to full.”

Aside from the cost of new construction, there’s also a public relations battle to consider. Packing plants already faced an uphill battle in the court of public opinion, something that certainly won’t be made any easier by the spread of COVID-19. There’s also the matter of getting a good location with access to animals and labor and securing the necessary environmental approvals for such a facility to run.

All told, a new beef packing plant – or a packing plant for any protein, for that matter – dreamed about today likely won’t be operational for another three years.

The nation’s pork sector is also in a bit of a different scenario than the beef industry, Lusk pointed out, and for a number of reasons. The herd had expanded in anticipation of potential exports to China, creating a glut of animals to be processed even if plant shutdowns weren’t a factor.

Steve Meyer, an economist for Kerns and Associates, says the industry is more than 2 million hogs behind in its processing endeavors, something that will result in a combination of euthanizing healthy hogs and seeing what plants can do to work through the backlog. But their ability to do so is rather limited.

“To get caught up, we’d have to operate everybody on Saturday for every Saturday for like three months, and that just kills your labor supply,” he said, pointing to an already difficult labor situation facing many plants.

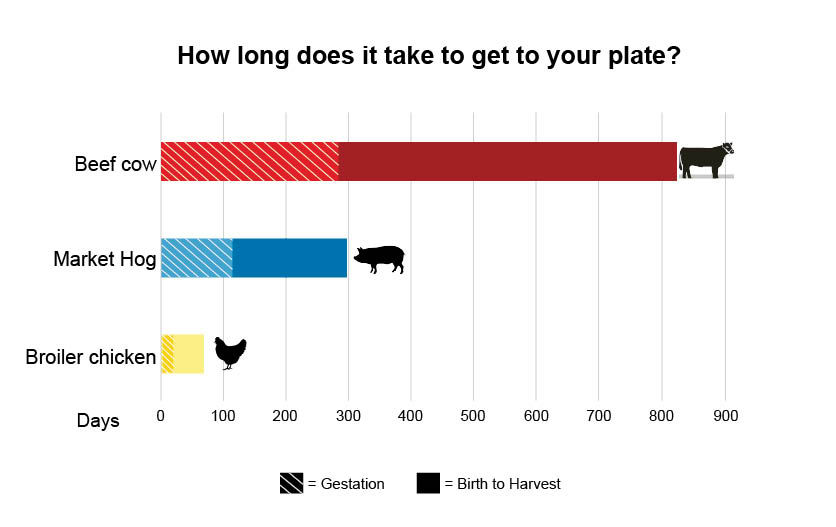

Pork farmers also face a more immediate slaughter timeframe. While beef cattle have the option to stay on feed for a little longer before needing to go to the plant, a market hog is set to be processed about 26 weeks after it is born (beef cattle are typically harvested after about 18 months). That quicker turnaround from birth to processing will also help the industry reassess its capacity, Meyer noted.

“I think we’re going to come out of this on the other side and have a several percentage – and I don’t know what to say on that yet – lower output, and that’s going to push prices up and probably encourage some growth,” he said. “I think two to four years down the road, we’ll find ourselves thinking maybe we need another packing plant. But one thing we did is we kind of outgrew the ones we built pretty quickly.”

But the protein with the quickest turnaround of all is poultry. Will Sawyer, a lead animal protein economist for CoBank, says the sector has consistently been expanding its processing capacity, something that won’t be slowed by the coronavirus.

“The capacity expansion situation within poultry I think is going to continue until these producers are facing a year, or maybe more than a year, of losses,” Sawyer told Agri-Pulse.

In an interview, Sawyer rattled off a number of facilities built in the last few years and planned to be built in the next. In fact, poultry slaughter is actually up year to date over 2019 figures, albeit at a lesser amount than it was after the first quarter.

According to the USDA data, American poultry processors harvested nearly 759 million chickens in April 2020 – just shy of 24.5 million birds per day, about 99% of the industry's April 2019 output.

Interested in more coverage and insights? Receive a free month of Agri-Pulse or Agri-Pulse West by clicking here.

But no matter when or where a new plant might be built, or what it might process, it still has to make money and be seen as an attractive investment, a view that might elude the packing sector for a little while.

“There’s sometimes a view that there’s all this extra money out there, there are dollars being left on the table,” Lusk said. “The truth is, these are hard-earned dollars. You make them in little, small amounts at a time. You lose money in parts of the year, and it’s kind of a long bet.”

For more news, go to www.Agri-Pulse.com.